Offshore investment is a method of investing in tax havens, where little or no taxes are imposed. It is possible to earn large yields by investing in offshore regions.

In this case, what we need to worry about is the investment yield. It is natural to want to know how much of an investment yield or dividend is possible.

However, the yield you get depends on who you apply from. If the IFA (Independent Financial Advisor) you apply from is different, the annual interest rate will vary many times. You also have to understand the fees, and the lower the commission rate, the better the investment yield will be.

So I will explain how to think about offshore investment and how to get excellent yield with superior investment performance.

Table of Contents

Yield as Simulated Cannot Be Achieved

It is true that you can achieve excellent investment returns when you start regular investments. In fact, an annual interest rate of over 10% can be achieved without any difficulty.

When you are considering offshore investment, your introducer or other people may show you a document explaining the simulation of achieving a 10% investment yield every year.

Try to think of this as meaningless. It would be nice if we could actually achieve these yields, but that is not going to happen. Some years are good, and some are not. Also, an annual interest rate of more than 10% means that there is risk involved.

Therefore, you need to know what’s really going on.

Investment Performance Varies by IFA

Which financial institutions (insurance companies) can you sign up with to achieve excellent investment returns? For example, there are several financial institutions for offshore investment, as follows.

- Investors Trust

- RL360°

- Premier Trust

- Metis

However, it is not possible to calculate a definite yield and dividend at the financial institution where you invest. This is because the investment performance will be completely different depending on which fund you invest in.

Financial institutions such as Investors Trust and RL360° are places where money is deposited, and they hold many investments.

For example, in your country, a brokerage firm will not manage your assets; instead, you will try to increase your assets by investing in funds that the brokerage firm has, such as global stocks, emerging country stocks, and real estate. In the same way, consider that the investment performance of the funds held by financial institutions will be completely different depending on which funds you invest in.

These funds are chosen by the IFA. When making an offshore investment, you must apply through an IFA, and it is the agent that decides which fund to invest in.

Therefore, it is important to consider that investment returns vary greatly depending on the IFA you sign up with rather than the financial institution you apply to. If the IFA (agent) is excellent, the investment returns will be excellent, and if the asset management is poor, you will not get much profit.

Check Past Performance for Yields, Dividends, and Annual Interest

When you are recommended to invest offshore, you need to check the past performance of the IFA. In fact, there are a lot of unmotivated agents who are poor at investing.

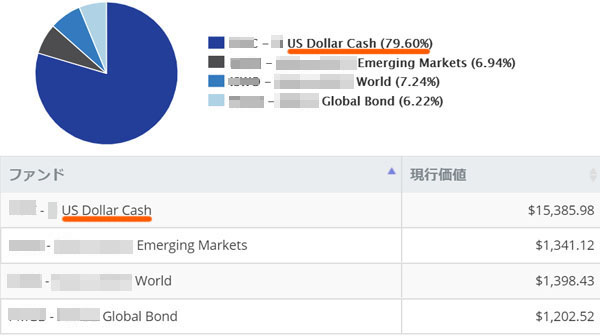

For example, in my case, the IFA set up the following portfolio for my first offshore investment contract.

As you can see from the fact that it says US Dollar Cash (79.60%), the money I had saved was not invested in the fund but was held as cash in my portfolio. Naturally, since it remained in cash, the money did not grow, and I lost opportunities for several years.

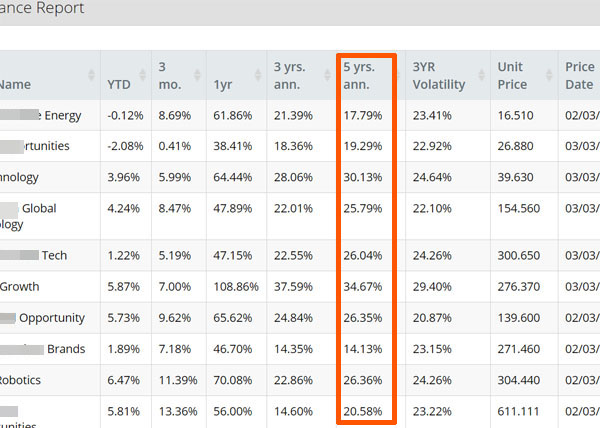

Since I could not see this situation improving, I switched to a new IFA. After that, the IFA reconfigured my portfolio to diversify into global and high-tech stocks, etc., as shown below.

For reference, the average annual interest rate of this portfolio over the past five years is 24.1%, which means that after changing the IFA, I have been able to earn a large investment profit.

After all, IFA is the most important factor in offshore investment. As for me, even though the financial institution I used was the same, by changing the IFA, the yield became more than 10 times higher than before.

The Minimum Annual Interest Rate for Principal Protection Is About 4%

There are also regular investment products that offer low-risk, steady investments, rather than aggressively investing in funds and aiming for annual interest rates of 10% or more.

There is a product called principal protection that guarantees future profits. In this case, you are promised that your assets will definitely increase in exceptional cases.

For example, one offshore financial institution offers a principal-protected financial product called the S&P 500 Index. In this investment product, as clearly stated on the official website, the minimum amount of asset management is assured depending on the investment period as follows.

- 15-year plan: 140%.

- 20-year plan: 160%.

The S&P 500 is an index that represents the stock prices of the 500 most advanced companies in the United States. With the S&P 500 Index offered by the offshore investment company, you will be 100% invested in the S&P 500.

160% in 20 years is possible with an annual interest rate of about 4%. Therefore, when investing in principal-protected financial instruments, regardless of the IFA you sign up with, you can be assured of a minimum yield that is almost fixed.

For reference, the annual interest rate of the S&P 500 is 7-9%. Therefore, the annual interest rate of 4% is a very low estimate, and the asset will actually increase at a higher annual interest rate.

The Lower the Financial Institution’s Commission, the Better

Dividend and investment yields vary greatly from IFA to IFA. For principal-protected financial products, the annual interest rate is exceptionally the same no matter which IFA you choose. Other than that, investment performance is entirely depending on the agent.

In addition to that, you also have to consider the fees of the financial institution.

In general, the fees for offshore investments tend to be high. Since offshore investments aim for high annual interest rates, you might think that high fees are not a problem. However, if the IFA is not good and the asset management is poor, the principal will be lost.

Also, even if the asset management is going well, if the commission rate is high, the investment profit will decrease. Therefore, the lower the commission rate, the better.

For example, when investing in stocks, it is common practice to use online securities. This is because it allows you to reduce the annual fees paid. In the same way, when you invest offshore, you have to choose a financial institution with the lowest commission rate.

Which Financial Institutions Have Low Commission Rates?

What kind of financial institutions can you invest in to get a low commission rate? As mentioned earlier, the main financial institutions we can sign up with are as follows.

- Investors Trust

- RL360°

- Dominion Capital Strategies

- Dominion Capital Strategies

- Premier Trust

- Metis

Of these, the insurance company with the lowest commission rate is Dominion Capital Strategies. Therefore, unless you have a special reason, you should choose Dominion Capital Strategies.

RL360° is another well-known company for regular investments. However, when compared to Dominion Capital Strategies, RL360°’s commission rates are much higher. Therefore, even if you invest in the exact same fund, your return on investment will be better with Dominion Capital Strategies than with RL360° because of the difference in fees.

In the case of RL360°, the overall commission rate is about 3%. Even a difference of 0.5% per year can make a difference of tens of thousands of dollars in investment income after 20 years. Therefore, you have to think carefully about the fees.

The financial institutions with the lowest commission rates for offshore savings investments have already been determined. It is essential to choose an insurance company with low commission rates, and you need to think about which IFA you purchase from.

Consider Both Annual Yield and Fees

When considering overseas savings investment, how much return you can get is a very important factor. However, there is no way to know about specific yields, dividends, and annual interest rates. This is because the financial institution does not manage your assets, but the IFA chooses which funds to invest in.

Think of the financial institution as a place to deposit your money, and the actual investment instructions are given by the IFA. Depending on the IFA, annual interest rates of over 10% may be possible, or your money may not grow at all.

On the other hand, some financial institutions of offshore investments offer low-risk products with principal protected. In this case, you will be able to increase your money by at least 4% per year.

However, even if you invest in the same fund, the investment profit will be completely different depending on the fees charged by the financial institution. Therefore, it is a good idea to use a financial institution with a low commission rate to invest in offshore funds.

There is a correct way to increase your assets through offshore investment. Make sure you understand how to manage your assets before choosing a financial institution to invest in and find a good IFA.

Related Posts

Compounding Effects of Investing in Stocks with Index Mutual Funds

Compounding Effects of Investing in Stocks with Index Mutual Funds- INDA Is a Recommended Mutual Fund and ETF for Indian Stocks

- Offshore Cryptocurrency Investment: Managing Your Assets in a Tax Haven

- Alternative Investments Made by Institutional Investors and Family Offices

- Advantages and Disadvantages of Investing in Hedge Funds

- Dominion’s PIP (Principal Protected) Structure in Offshore Investment